📈 Dataset: Cloud provider concentration across 67,813 companies — useful for portfolio due diligence. Raw numbers at cloud.awsexpansion.com/api/stats.json (opens JSON endpoint).

Here’s a risk factor that appears in very few LP due diligence packets: portfolio-level cloud concentration.

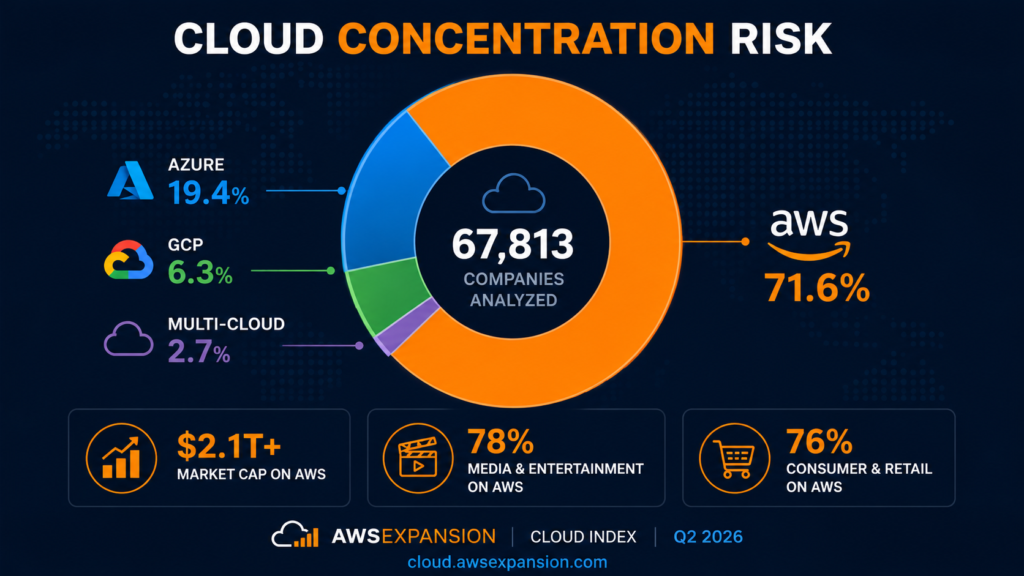

As of Q2 2026, 71.6% of enterprise companies with detectable cloud infrastructure run on Amazon Web Services. That figure — from the AWSExpansion Cloud Index, which tracks 67,813 companies via infrastructure signal analysis — represents something specific for institutional investors in technology: a large and growing share of enterprise software value is directly exposed to a single infrastructure provider’s pricing decisions, service outages, and strategic choices.

This isn’t necessarily a problem. But it’s worth understanding.

The Scale of AWS Dependency in Enterprise Tech

The AWSExpansion dataset provides a useful lens. Among the 9,522 confirmed AWS companies in the tracked universe, the public companies alone represent over $2.1 trillion in combined market capitalization — dwarfing the $890B market cap sitting on Azure and $420B on GCP.

The concentration is not uniform across sectors. Media and Entertainment (78% AWS), Consumer/Retail (76%), and Technology companies (73%) show the highest AWS dependency. Healthcare shows the lowest AWS concentration (64%) and the highest Azure presence (28%).

For a venture fund with significant exposure to SaaS and cloud-native infrastructure companies, this means: the majority of portfolio companies are likely running on AWS, and therefore share correlated infrastructure risk.

Three Risk Vectors to Understand

Pricing risk. AWS has historically raised prices modestly and selectively. But the market position is undeniable: a company running deeply on AWS Lambda, RDS, and S3 — where migration to GCP or Azure would require significant re-architecture — is exposed to vendor pricing leverage. At the portfolio level, an AWS-wide price increase affects a disproportionate share of tech company operating costs simultaneously.

Outage correlation. AWS outages are infrequent but market-moving when they happen. A major US-East-1 disruption takes down a correlated set of portfolio companies simultaneously — not because of specific vulnerabilities but because of shared infrastructure. This concentration risk rarely shows up in traditional portfolio construction frameworks.

Strategic dependency. As AWS builds more services that compete with the software layers above them (database, analytics, AI/ML, security), portfolio companies running on AWS face a nuanced risk: their infrastructure provider is also their most capable potential competitor. The competitive dynamics are different from, say, a dependency on Azure where Microsoft’s software ambitions are more concentrated in productivity and enterprise.

The Upside Side of Cloud Concentration

To be clear: AWS concentration is not inherently negative from an investment standpoint. Several positive correlates exist:

AWS Marketplace as a distribution channel. Companies listed on AWS Marketplace gain access to AWS’s enterprise customer relationships, co-sell programs, and committed spend drawdown (EDP) arrangements. The concentration of enterprise buyers on AWS creates a network effect for AWS-ecosystem software vendors.

AWS partnership alignment. The 9,522 confirmed AWS companies in the AWSExpansion dataset are the warm market for any AWS-adjacent ISV. Portfolio companies with strong AWS alignment have a clear, well-defined TAM that’s growing.

Ecosystem network effects. When 71.6% of your target customers run on the same platform, integration investments compound. A single AWS-native integration reaches the majority of the addressable market.

What the Multi-Cloud Minority Tells Us

Only 354 companies (2.7% of detected) in the AWSExpansion dataset genuinely run multi-cloud. From an investment perspective, this cohort is worth understanding separately.

Multi-cloud companies tend to be large, compliance-driven, or post-acquisition — not early-stage. They’re more operationally complex, which creates opportunity for infrastructure management tooling. But the “multi-cloud by default” strategy that some infrastructure vendors pitch to investors as a TAM expansion story doesn’t match the underlying adoption data.

Due Diligence Implications

For investors evaluating technology companies, the AWSExpansion Cloud Index provides a free way to verify cloud infrastructure claims and contextualize them against sector norms. If a company claims their target customers are “cloud-first” without specifying which cloud, the data suggests AWS is the safe prior — which has implications for integration priorities, go-to-market alignment, and competitive positioning against Amazon’s own service expansions.

The full dataset is searchable by sector, geography, and company size at cloud.awsexpansion.com.

AWSExpansion Cloud Index Q2 2026. Market cap figures are aggregate public market capitalization estimates based on companies in the dataset. Not investment advice. Methodology at cloud.awsexpansion.com/report.html

Assess cloud concentration risk in your portfolio. The AWSExpansion directory covers 67,813 companies with cloud provider data.Run a Portfolio Check →